A majority of Americans are in debt. Maybe that statement doesn’t surprise you, because chances are that you’re part of that majority. There’s a reason I say that, and it’s not that I’m just trying to generalize.

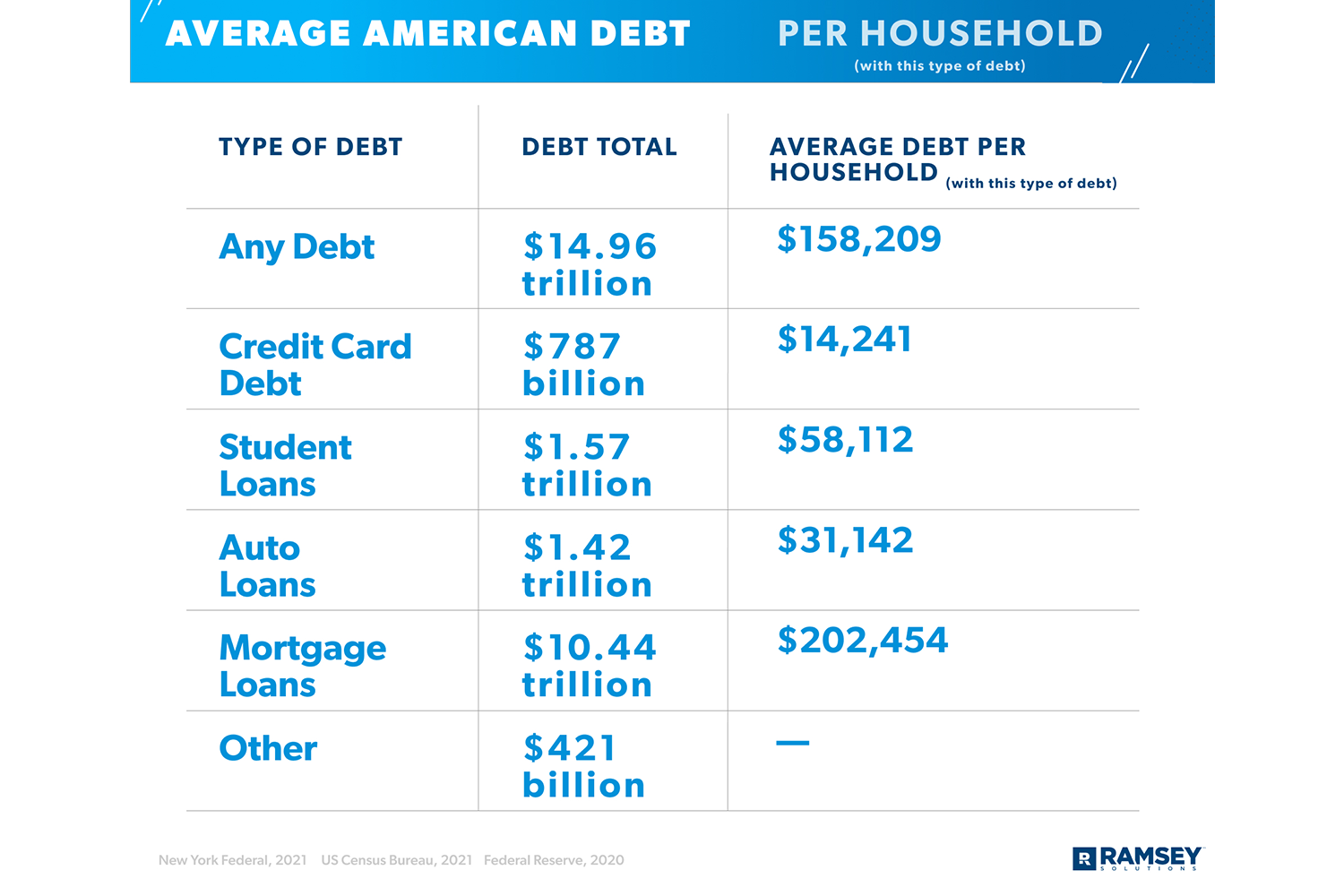

The fact of the matter is that 77% of American households have some kind of debt. But just how much do these households owe? Let’s put some dollar figures to that statistic.

The total of any debt in the United States is $14.96 trillion. According to Ramsay Solutions, this is an average of $158,209 per household. Mortgage loans make up the majority of debt, followed by student loans, then auto loans, and finally credit card debt. There are other costs as well, but these are the most common.

via Ramsey Solutions

Of course, people can manage these by making consistent payments to the organization they owe. For instance, homeowners make monthly mortgage payments to their lenders.

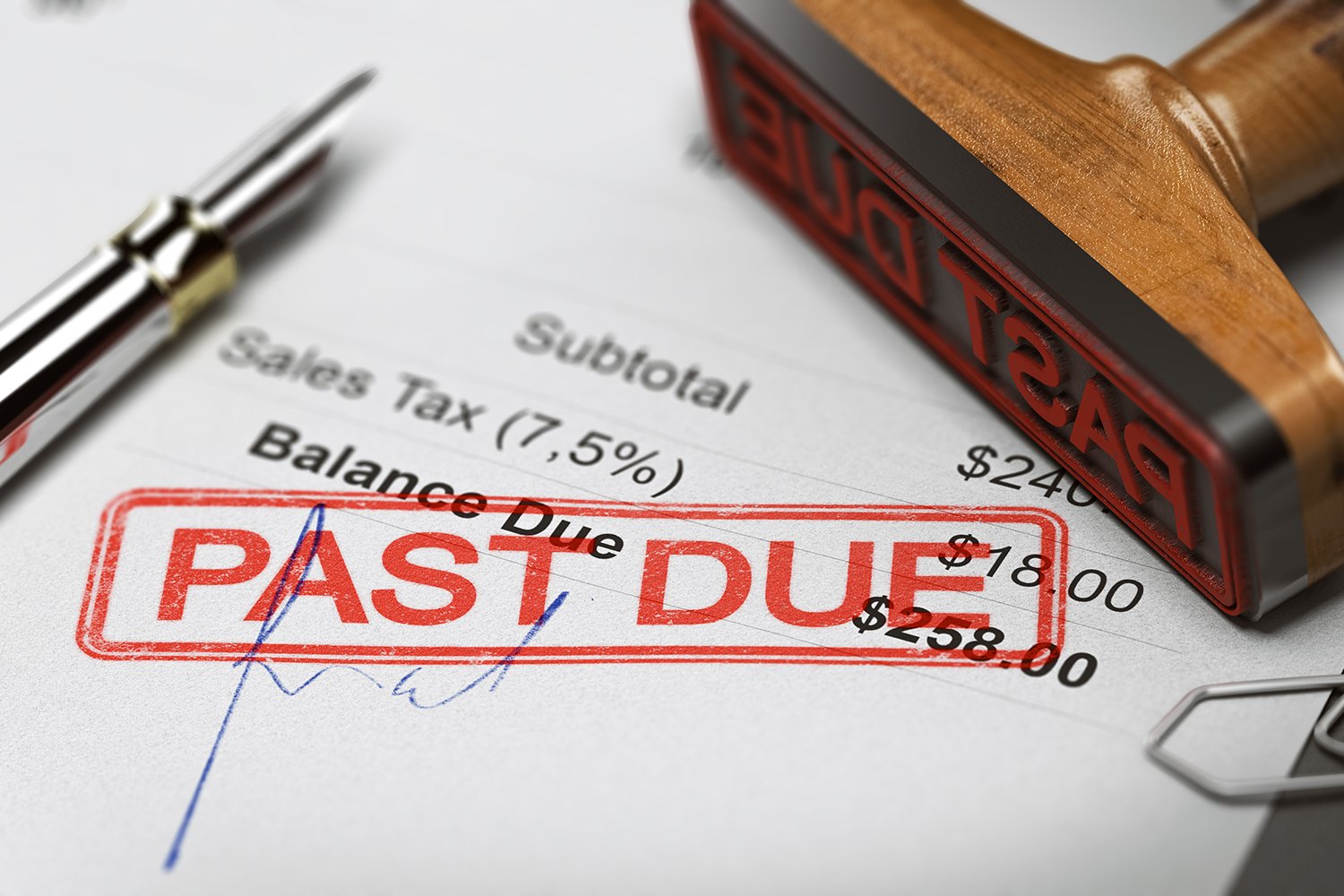

These bills become problematic when the borrower misses a payment or stops making them altogether. No one wants to end up in that situation, but the reality is that it can be hard to keep up with too many payments. This results in one-quarter of Americans who don’t pay their bills on time.

Enter: debt collectors. If you’re reading this blog, then you most likely know what these people do. You might even be one yourself.

But just in case you stumbled here looking for the definition, let me summarize. Debt collectors do exactly what it sounds like they do…collect debts. If a borrower doesn’t pay their bill, then the collector buys these past-due payments from the business or creditor. They then try to collect what the person owes.

To do this, they send debt collection letters. Put simply, these remind an individual that they owe money. The goal is that the person will finally pay, especially now that their bill is in the hands of a collection agency. After all, no one wants to deal with any potential legal action.

I’m sure you can agree. Even as a debt collector, you don’t want to handle potential lawsuits. But how do you get people to pay before it gets to that point?

Writing an effective yet ethical letter is the first step to initiating this process. You might be wondering what exactly I mean by “ethical.” It’s more than just writing a polite letter. As a debt collector, there are legal requirements that you need to follow.

If I had to guess, most people aren’t missing their payments simply because they don’t feel like paying. A more probable reason is that they have financial difficulties making it impossible to afford. Because it’s a sensitive situation, the government offers protections for people when it comes to collection agencies’ attempts to get their money.

The Fair Debt Collection Practices Act protects individuals from inappropriate and abusive behavior from debt collectors. This law states that collectors can’t…

Lie about who they are, the amount owed, or potential outcomes

Use abusive practices or harass the debtor

Threaten to hurt the person

Use obscene or profane language

Repeatedly call or text the person

Treat the person unfairly

Tell anyone else about the money owed other than the debtor’s spouse

Contact a debtor before 8 AM and after 9 PM unless the individual agrees

Contact the person at work if they said they can’t receive calls there

Continue contacting the person after they’ve written a request to stop

There’s a movie from 2009 called Confessions of a Shopaholic. The main character, Rebecca Bloomwood, owes a debt collector thousands of dollars. The collector, Derek Smeath, violates so many of these rules. He harasses her by repeatedly calling her personal and work phone, and he shows up at her apartment and place of work.

In one scene, Bloomwood is a guest on a talk show on live television. She doesn’t know that Smeath is in the audience. When the talk show host asks the audience for questions, he exposes Bloomwood’s debts in front of the entire audience and on live television.

Of course, the film is a comedy so they don’t focus on how he was breaking so many rules that the FDCPA would have protected her from. But it’s a good example of what collection agencies shouldn’t do.

So now that you know the ethics behind contacting those who owe money, here are four effective debt collection letter examples that you can use.

Table of Contents

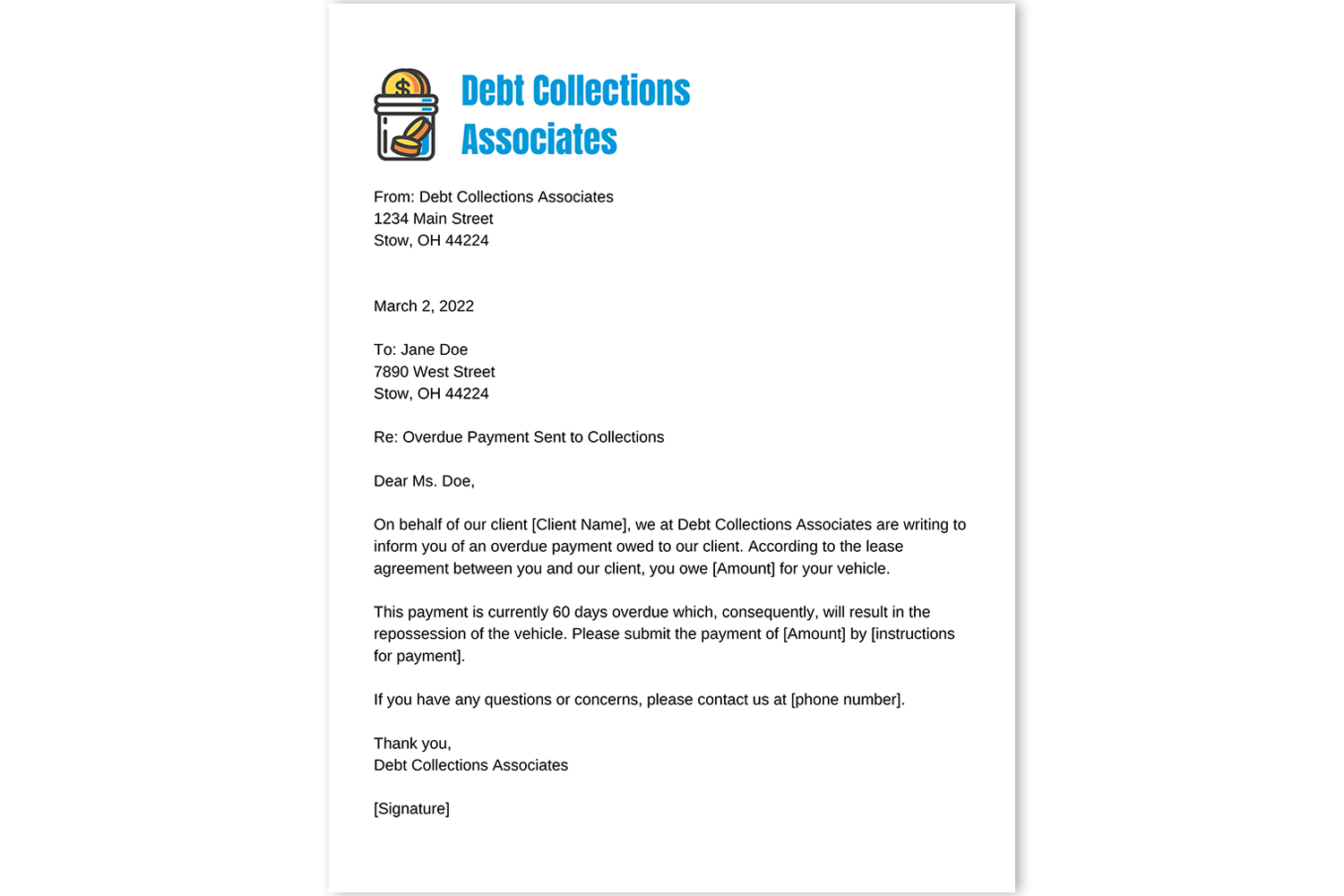

General Notice Letter

People likely already know that they owe money since they would’ve received a bill before it went to collections. Although, they might not know what the time frame is before this transfer happens.

The time it takes for an account to go to collections differs for lenders, creditors, and even by state. For example, Georgia’s foreclosure process period is just 37 days while New York’s can take up to 445 days. That difference is significant: a little over a month, versus well over a year.

Repossession on car loans usually starts by 60 days. Credit cards on the other hand usually go to an in-house collection department before going to a formal collection agency.

You get the point. Various factors contribute to the timeline for when a debt collector gets involved.

This is why you need to send an initial letter stating that you’re now responsible for collecting payment.

The sample above includes a space for the agency to state who they’re collecting on behalf of. This way, the person who owes knows why they’re receiving the letter. By including the amount, deadline, and instructions to pay, this individual knows how to settle their balance without facing the stated penalty.

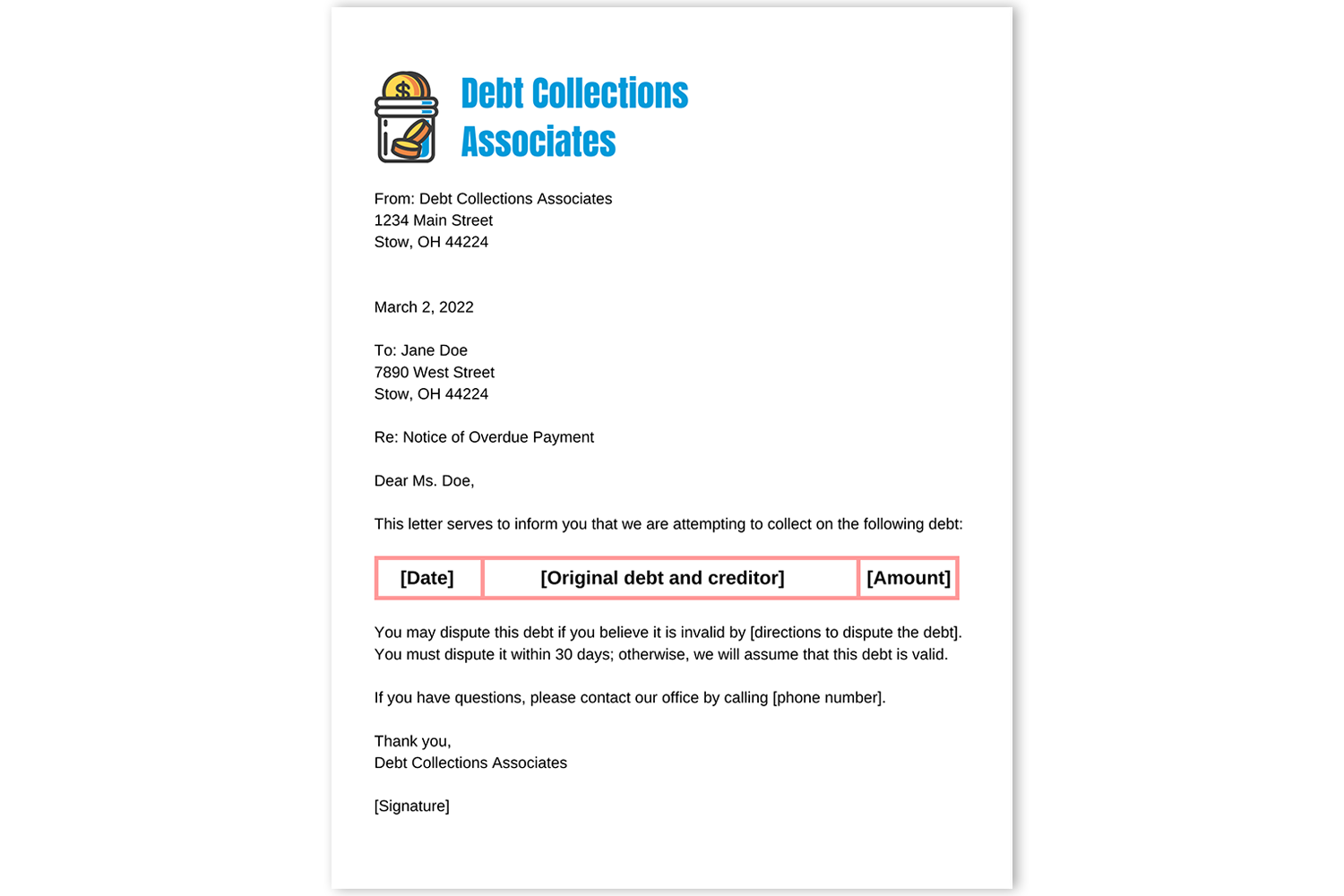

Required Validation Letter

It’s a requirement that debt collectors send a validation letter within five days of first contacting an individual. These most likely include some of the same information as the initial debt collection letter example in the previous section.

However, there are a little bit more details that they need to include to qualify as a validation letter. By law, they must state…

The name of the creditor/business that the person allegedly owes

The amount owed

That the individual has the right to dispute the debt and must do so within 30 days

If the person makes a dispute, then the collector must provide written evidence of the debt.

Depending on how you structure the first letter you use to contact an individual, you might not need to send an entire separate validation letter. As long as the initial one includes the required details by law, you’re all set.

You’ll most likely end up sending a letter specifically for this reason if you first contact the person by phone. Since they don’t yet have the information in writing when you call, you must send it to them within five days.

Payment Plan Option

As I already mentioned, a reason why many debts go unpaid is due to financial difficulties. For instance, over 25% of Americans struggle to afford their medical bills. And over half of those people have no other debts besides these medical bills.

Because of the financial challenges, payment plans are a helpful way for both the person who owes and the organization that’s collecting. Since the person has avoided paying their bill for so long, they still might not have the money by the time it reaches collections.

Offering a way for them to make payments in increments helps them decrease their debts over time. Sure, it might not be the full amount that they owe you. But a little is better than nothing, you’ll receive the full payment eventually, and it isn’t as much of a hassle as going to court.

These plans will also help ease the anxiety that people have surrounding bills. 72% of Americans stress about money each month. So if they’re able to break up how much they owe at one time, it becomes more manageable.

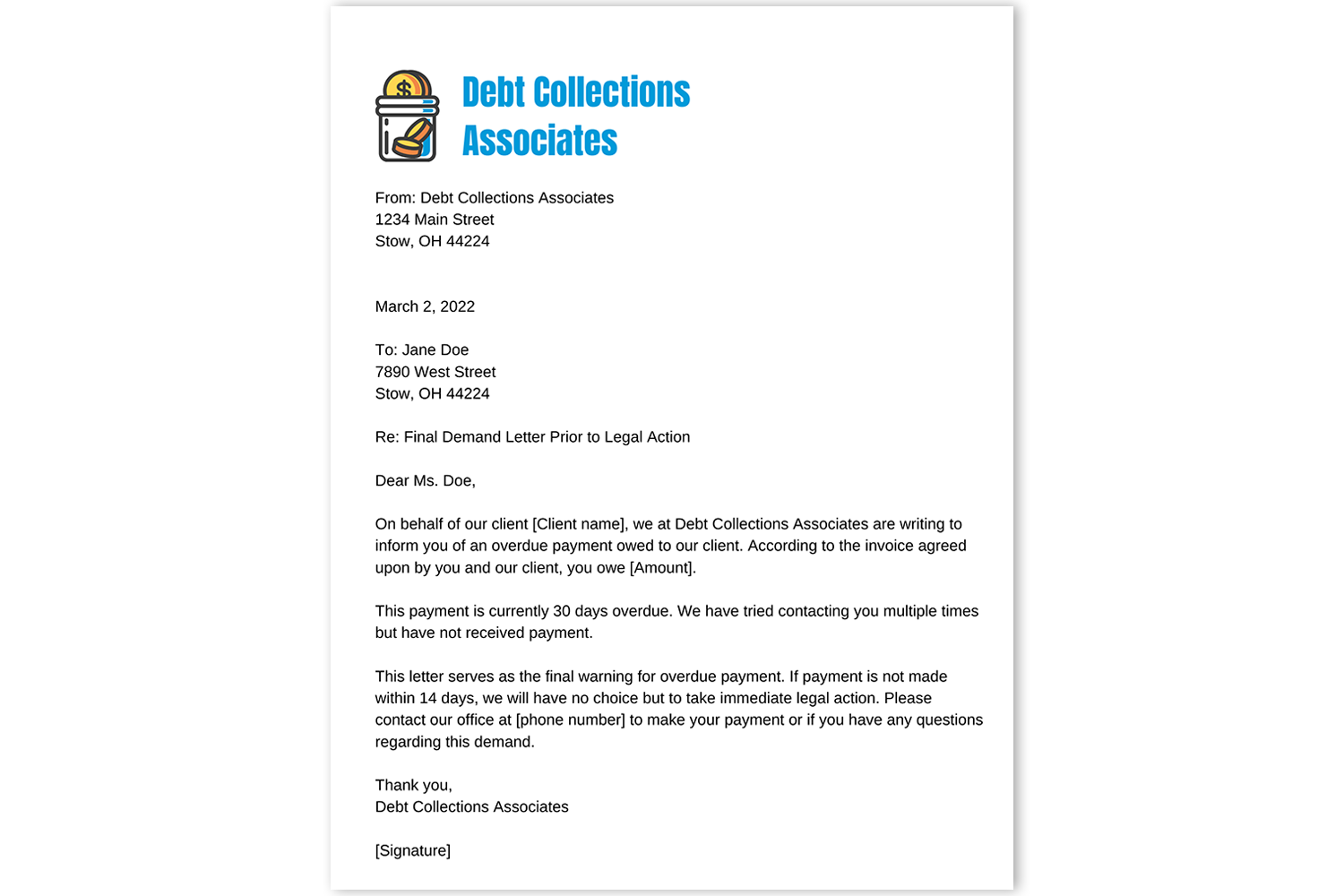

Final Demand Before Legal Action

Sometimes you have no choice but to take legal action. No matter what you try, you just can’t get the individual to pay.

It’s not like you can keep calling them until they’re so annoyed that they finally pay you. After all, that would go against the FDCPA. So what do you do?

You write a letter stating that this is their final chance to pay before you take legal action. This often gets referred to as a demand letter.

These shouldn’t come off as threatening, since the FDCPA protects people against threats. Instead, state that you’ve tried contacting them already, you have no choice but to pursue legal action, and that they can contact you with any concerns or questions.

Hopefully, this is enough to get their attention so that they’ll settle their bill before you have to go to court. But unfortunately, that’s not always the case. If they deny your claim that they owe money or they ignore the letter altogether, then you can take legal action by bringing the lawsuit to court.

In some situations, the recipient may request that you only contact their attorney. If that happens, then you must oblige unless their attorney fails to respond to you within a reasonable timeframe.

Conclusion

Since debt is such a common issue, it isn’t unlikely that people will occasionally struggle to pay their bills on time. Making a payment a few days late until the next paycheck hits the bank is one thing.

But for it to turn into a month or longer is another story. When this happens, the organization that the person owes will likely send the account to collections. From there, the debt collector gets involved.

Since they likely won’t want to pursue legal action right away, they make the effort to get money from the debtor. After all, no one wants their credit damaged from their account going to collections.

Approaching those who owe money is a sensitive situation. There are most likely financial challenges involved, hence why it’s taking so long for them to pay. To protect these people from potentially abusive collection tactics, the government requires collectors to abide by certain practices.

So when these professionals write their letters to get payment, they need to structure them carefully. By following the tips of these debt collection letter examples, they’ll be sure to use effective and ethical practices.