This article is a part of your HHCN+ Membership

The U.S. Centers for Medicare & Medicaid Services (CMS) effectively went to war with home health providers when the agency unveiled its 2023 proposed payment rule on June 17. At the heart of the conflict is differing views on how the Patient-Driven Groupings Model (PDGM) has impacted the industry.

Ultimately, CMS estimates that its proposal would slash aggregate home health payments by 4.2%, or $810 million, next year. The figure takes into account a 2.9% Medicare payment increase, plus a 6.9% cut aimed at balancing out PDGM and another 0.2% cut related to outlier payments.

If the agency moves forward with its plan, the ramifications on the home health market could be profound.

In particular, I see two clear consequences: a downturn in transaction activity and decreased investment in care innovation. The proposal itself may even be unfavorable enough where providers and investors already shift to more bearish mindsets in these areas, regardless of what happens with the final rule released in fall.

“What we see in the proposed rule is the equivalent of a declaration of war against home health agencies and the 3-plus million patients they serve,” National Association for Home Care & Hospice President William A. Dombi wrote in a report to the advocacy organization’s members. “To believe this will have no impact on patients is to live in a bubble.”

In addition to PDGM and potential payment adjustments, the 2023 proposed rule also included interesting nuggets from CMS around therapy utilization and health equity within the home health setting. The proposal likewise included relatively minor tweaks to the Home Health Value-Based Purchasing (HHVBP) Model, which is rolling out nationwide come Jan. 1.

I offer some of my key takeaways from the proposed payment rule in this week’s exclusive, members-only HHCN+ Update.

Maintaining budget neutrality

As mandated by Congress, PDGM must be budget neutral, meaning payments to home health agencies under the current reimbursement methodology must be equal to what they would have been under the old Prospective Payment System (PPS). PDGM went into effect Jan. 1, 2020.

Home health stakeholders and CMS both agree that PDGM hasn’t been budget neutral, but that’s about where they stop seeing eye to eye. Using a method that “simulates” what payments would have been if PPS remained in place while simultaneously adjusting for the COVID-19 pandemic, here’s how CMS says PDGM played out in its first two years:

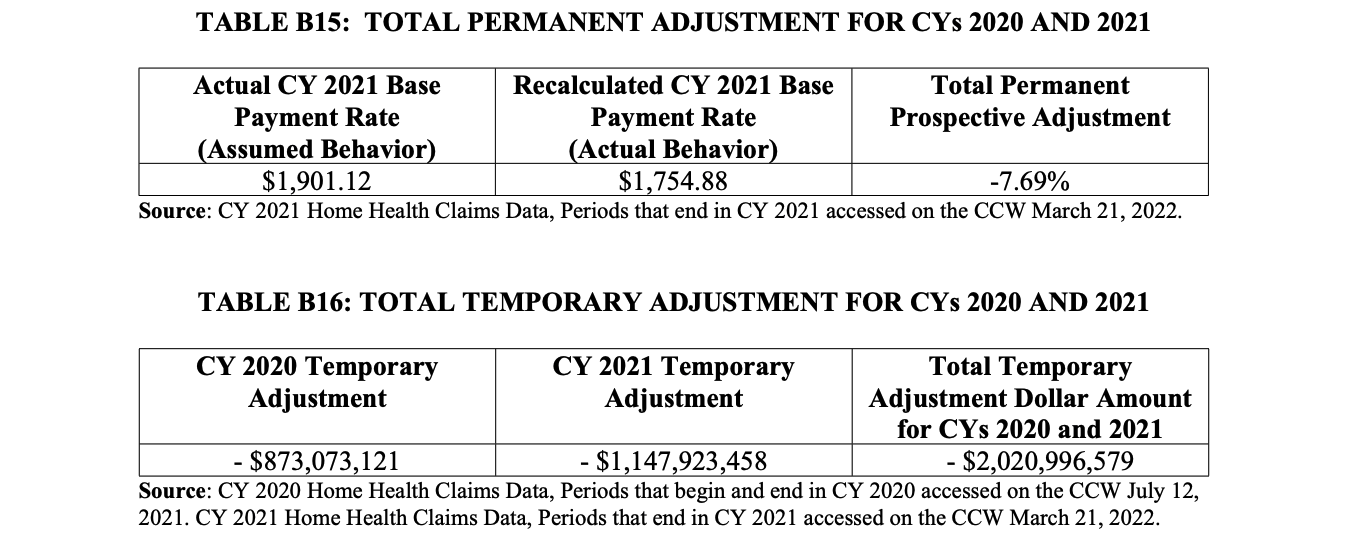

– In 2020, CMS determined that its initial estimate of base payment rates required to achieve budget neutrality resulted in excess home health expenditures of approximately $873 million.

– In 2021, CMS determined that its initial estimate of base payment rates required to achieve budget neutrality resulted in excess home health expenditures of approximately $1.1 billion.

In total, CMS estimates that the agency overpaid home health providers by $2.02 billion in 2020 and 2021 – overpayments it is eventually obligated to “reconcile.” And to balance PDGM moving forward, CMS believes it needs to implement a permanent downward adjustment of 7.69% to the CY 2023 base payment rate.

Again, the home health industry widely refutes the idea that PDGM has resulted in a windfall compared to PPS. While CMS says PDGM led to hundreds of millions of dollars in overpayments in 2020, for example, industry data – gathered by outside consulting firms – says the overhaul actually led to payments being 2.5% lower than they should have been.

“Reliable analyses prove that PDGM underpaid home health agencies,” Dombi continued in NAHC’s report.

For context, CMS initially called for a downward behavior change adjustment of 8.39% to the base payment rate in 2020. Based on comments the agency received in the rulemaking process, it lowered that to a downward adjustment of 4.36%.

In its proposed rule, CMS seeks to immediately enact the full permanent payment adjustment while holding on any retrospective clawbacks.

“We recognize that applying the full permanent and temporary adjustment immediately would result in a significant negative adjustment in a single year,” the agency wrote. “However, if the PDGM base 30-day payment rate remains higher than it should be, then there would likely be a compounding effect potentially creating the need for a larger reduction in future years.”

Potential ramifications

Home health transaction volumes began to dip toward the end of last year and remained down in early 2022, according to data from M&A advisory firm Mertz Taggart. Several factors are influencing buyers and sellers alike, including staffing challenges and HHVBP expansion, as well as rising inflation and interest rates.

Aggregate home health payments decreasing 4.2% next year would certainly temper M&A expectations going into 2023. But just the specter of cuts could also be enough to steer private equity buyers away from home health dealmaking and cause strategic buyers to deploy capital more conservatively.

Kris Novak, senior vice president of M&A at Amedisys Inc. (Nasdaq: AMED), suggested as much at Lincoln Healthcare’s Home Care Innovation and Investment Conference this week.

“The proposed rule will certainly throw water on things for the next couple of months,” Novak said during a panel discussion. “We’ll have to see what happens when the final rule comes out, but I think it’s going to be a slow go [for transaction activity].”

The last time CMS proposed and finalized cuts to the home health industry was 2018.

Beyond M&A, cuts in 2023 could stifle innovation at a time when home-based care is playing a greater role in the broader U.S. health care system.

As the home health patient population has become more complex, providers have invested in training programs, partnerships and technology allowing them to deliver higher-acuity care. That was among the reasons Amedisys acquired Contessa Health last year and why others launched dedicated palliative care service lines.

If CMS tightens the Medicare wallet in 2023, forward-looking operators will, as a result, be able to take fewer chances or explore new territory.

“The investment community has felt that health care policymakers, government payers and managed care payers have all been in alignment with the view that increasing access to home-based care and home health is a positive attribute for the health care system,” Scott Fidel, an analyst at the private investment banking company Stephens, recently told HHCN. “There’s a real struggle right now with the message that CMS is sending here.”

Additional observations

The proposed rule wasn’t just about rebalancing PDGM, however. The below also stood out to me as areas providers should keep an eye on.

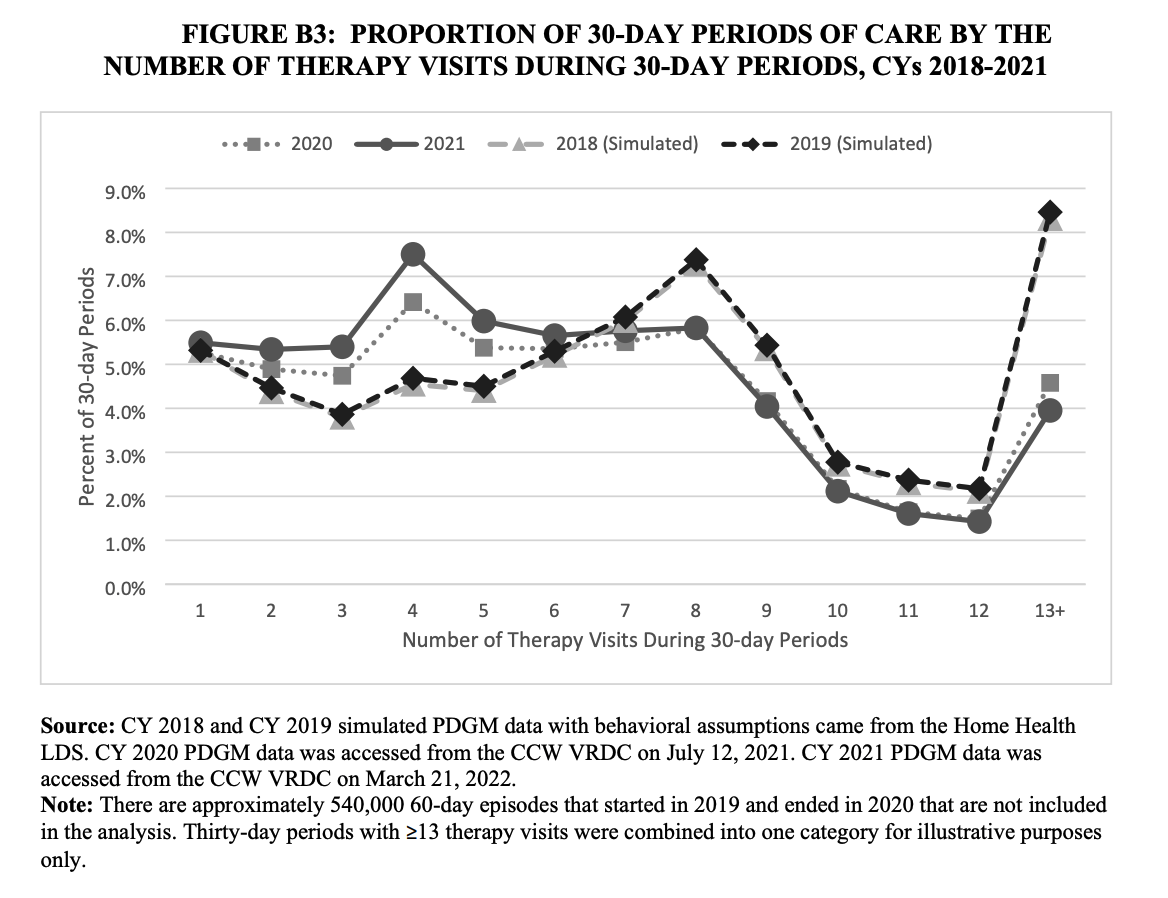

Therapy still under the microscope: Following PDGM’s implementation, many expected therapy utilization to drop, as reimbursement was no longer directly linked to visit volume. CMS data suggests that did, indeed, happen.

“Commenters stated that there has been a large decrease in therapy utilization since the implementation of the PDGM,” CMS wrote in the proposed rule. “Commenters stated several possible reasons for the decrease in therapy utilization, including that the PDGM resulted in significant differences in payment incentives.”

No major HHVBP adjustments: HHVBP is set to begin next year, but many have pointed out perceived flaws to the model’s design. Some, for example, claim it’s inherently unfair to have providers compete nationally instead of on a state or regional level. Others argue HHVBP fails to take into account social determinants of health (SDoH) or cases where a patient’s condition is unlikely to improve.

CMS did not suggest any significant structural changes to HHVBP in its proposed rule. Instead, it proposed:

– Adding definitions for home health agency baseline year and Model baseline year, and removing the previous definition of baseline year

– Changing the home health agency baseline year from CY 2019 to CY 2022 for existing agencies with a Medicare certification date prior to Jan. 1, 2019, and from 2021 to 2022 for agencies with a Medicare certification date prior to Jan. 1, 2022 starting in the CY 2023 performance year

– Changing the model baseline year from CY 2019 to CY 2022 starting in CY 2023 (to “enable CMS to measure competing [agency] performance on benchmarks and achievement thresholds that are more current”)

The overall economic impact of the expanded HHVBP model for CYs 2023 through 2027 is an estimated $3.4 billion in total savings to fee-for-service Medicare, mainly from a reduction in unnecessary hospitalizations and skilled nursing facility (SNF) usage as a result of greater quality improvements in the home health industry. As for payments to agencies, there are no aggregate increases or decreases expected to be applied to those competing in the expanded model.

Continued focus on health equity: CMS also explained that it’s seeking stakeholder feedback on its work around health equity measure development for the Home Health Quality Reporting Program (QRP), and the potential future application of health equity in the expanded HHVBP model’s scoring and payment methodologies.

As it related to the QRP, the agency is seeking stakeholder feedback on the following questions:

– What efforts does your HHA employ to recruit staff, volunteers, and board members from diverse populations to represent and serve underserved populations? How does your HHA attempt to bridge any cultural gaps between your personnel and beneficiaries/clients? How does your HHA measure whether this has an impact on health equity?

– How does your HHA currently identify barriers to access to care in your community or service area?

– What are the barriers to collecting data related to disparities, SDOH, and equity? What steps does your HHA take to address these barriers?

– How does your HHA collect self-reported demographic information such as information on race and ethnicity, disability, sexual orientation, gender identity, veteran status, socioeconomic status, and language preference?

– How is your HHA using collected information such as housing, food security, access to interpreter services, caregiving status, and marital status to inform its health equity initiatives?

CMS is also considering the adoption of a structural composite measure for the Home Health QRP related to health equity.